Blockchain technology is relatively young. Bitcoin leveraged decentralised ledger technology back in 2008, and in the early years, only a few people were aware of it.

Since then, many other projects have adopted this technology, with varying degrees of success. Often, projects don’t go past a proof of concept, and even if they do, the outcome might not be what the project’s proposers intended. It is safe to say that blockchain, as a technology, has not reached maturity.

There are multiple reasons why a blockchain project might fail, or yield a low return on investment (ROI). These reasons include, but are not limited to:

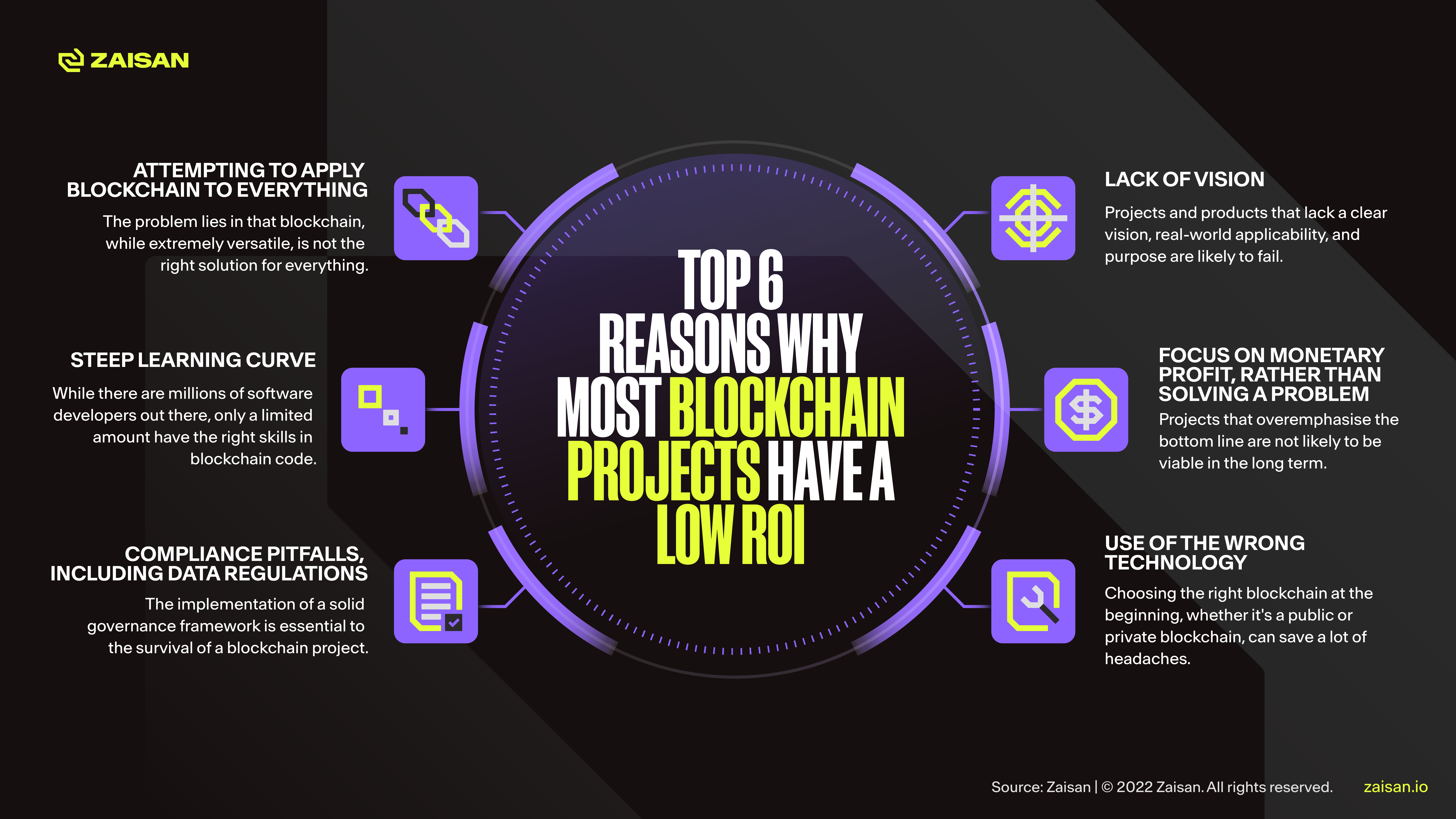

- Attempting to apply blockchain to everything

- Steep learning curve

- Compliance pitfalls, including data regulations

- Lack of vision

- Focus on monetary profit, rather than addressing and solving a problem

- Use of the wrong technology

This article explores the circumstances that often lead to blockchain projects having a low ROI, and how this can be overcome.

1. Attempting to apply blockchain to everything

Decentralised ledger technology does have the capacity to disrupt a fair amount of industries, and in fact, it has already done so, and will likely continue along this path of disruption and innovation for years to come.

But the problem lies in that blockchain, while extremely versatile, is not the right solution for everything. Fledgling entrepreneurs often use it as a buzzword and believe that blockchain will suit their projects, no matter what. Making this assumption without a proper assessment and due research is unwise, to say the least.

Adopting blockchain technology is a decision not to be taken lightly, and so entrepreneurs, or any business considering the implementation of a decentralised ledger, should look inward and look for the answer to these questions:

Is the legacy system no longer fit for purpose? Has it become too antiquated or expensive to maintain or update? Does the company have a way to obtain reliable data that can be fed into the blockchain?

Even if the answers to these important questions suggest that blockchain technology might be a suitable solution, the implementation of a blockchain network is not for the short term. Businesses must carefully consider the long-term implications, in terms of scalability (will the system be able to scale and accommodate higher numbers of transactions), complexity (does the company have the expertise to implement and maintain the technology), and ongoing costs (more nodes, bandwidth, etc.).

2. Steep learning curve

Blockchain technology does require a certain level of expertise. A blockchain is not an off-the-shelf product. Often, they require practical knowledge and expertise in certain programming languages that are specific to a blockchain (Solidity for Ethereum is a prime example of this). While there are millions of software developers out there, only a limited amount have the right skills in blockchain code.

In addition to this, the implementation of a decentralised ledger requires expertise in cryptography, smart contract programming, and very importantly, a functioning governance system. The combination of all these factors means that creating and maintaining a thriving blockchain ecosystem does require a steep learning curve.

3. Compliance pitfalls, including data regulations

Regulatory compliance can be defined as the acceptance, understanding, and commitment to follow all state, federal, and international laws and regulations that might be applicable and relevant to a company’s operation.

Blockchain compliance is therefore a hugely important issue for any business. Adhering and complying with local legal frameworks and regulations helps protect the company’s resources, uphold its brand reputation, and ensure that the company can remain in operation across different markets.

Blockchain technology has often found itself at odds with compliance guidelines, particularly in relation to privacy and data sharing, governance, and storage. The implementation of a solid governance framework is essential to the survival of a blockchain project.

4. Lack of vision

Entrepreneurs who decide to start a blockchain project just because it is fashionable or because they believe they can make a quick buck are probably doomed from the start. Blockchain is not a buzzword, nor is it a silver bullet that will magically make a product or project succeed. Establishing a thriving blockchain ecosystem is the result of a lot of work by a team of skilled professionals. Lacking a proper vision as to what the project or product should be, its real-world applicability, and the use case it fulfills is likely to lead to failure.

5. Focus on monetary profit, rather than addressing and solving a problem

Some entrepreneurs are out to make money, and though financial profit is of course necessary to stay in business, it should not be the primary objective. Projects that overemphasise the bottom line are not likely to be viable in the long term. A blockchain project must provide a real solution for a real problem, rather than manufacturing a non-existent problem to justify the use of a blockchain.

6. Use of the wrong technology

There are many blockchains out there: Ethereum, Bitcoin, Hyperledger, Corda, etc. Often, projects simply use the first one that comes to mind, which is usually Ethereum. Then the realisation sinks in that the gas fees can become incredibly expensive, which means that a business case becomes unreachable.

In this case, it is often difficult and costly to switch to another blockchain that facilitates a project’s needs better. And while tools such as an Ethereum Virtual Machine (EVM) can make it easier to switch to another more suitable blockchain. Picking the right blockchain at the start, whether it’s a public or private blockchain, can save a lot of headaches.

Conclusion

Issues like lack of compliance or clear vision, technological challenges, or poor planning can lead to a low ROI, or scupper a blockchain project altogether. It is up to the project creators to take all these factors into account and ensure that the use of blockchain technology is both justified, and sustainable. Because after all, blockchain technology, while a very powerful and versatile tool, cannot function on its own. It requires technical expertise and the right leadership to become a success.

Key takeaways

- Blockchain technology is not the answer to every single use case out there

- Decentralised ledgers do have a steep learning curve, which might lead to low ROI

- Using the wrong blockchain technology can have disastrous results

- Legal departments must ensure that blockchain networks are compliant with data sharing and storage regulations

- Blockchain projects require a clear vision of the objectives to accomplish

- Monetary profit must be supported by the resolution of real-world problems

- Projects must conduct careful research to ensure they choose the right blockchain technology for their use case

Zaisan is a web3 system integrator and start-up studio that provides the expertise and support to ensure blockchain-driven projects overcome all of these potential issues.